Double entry bookkeeping with variable chart of accounts Here's how it works

Jul 3, 2026•Channel

AI Analysis

Data from YouTube Data API v3•Updated Just now

Video Overview

Video Details

Published1 week ago

Duration15:27

Video IDJeP58mdijnU

Languageen

CategoryScience & Technology

PrivacyPublic

Made for KidsNo

Video TypeRegular Video

Performance Metrics

Views26

Likes0

Comments0

Engagement Rate0.00%

Likes per 100 views0.00

Comments per 1K views0.00

Video Tags

Description

Page:

https://excel.hpage.com/bookkeeping.html

Playlist:

https://www.youtube.com/watch?v=JeP58mdijnU&list=PLKnGGx0Hz5xI

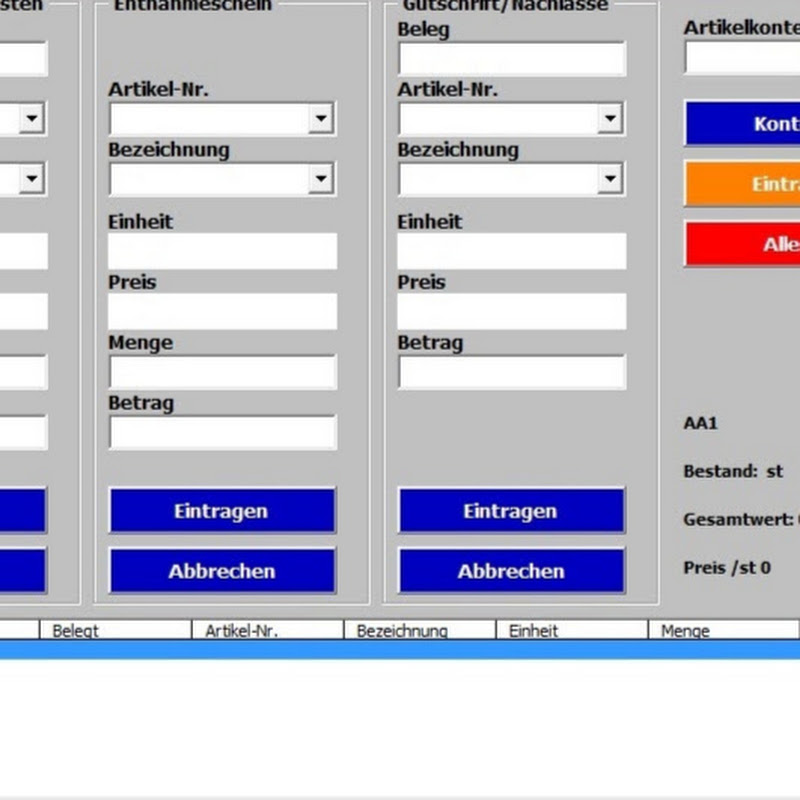

There are only three types of accounts here: inventory accounts, income accounts, and expense accounts. Users can create 224 accounts for each type. The names of created accounts can be changed at any time, and created accounts can also be deleted.

Here, users can create a list of buking texts; when recording a transaction, the description is selected from the list rather than being entered manually.

There is no distinction here between asset and liability accounts; instead, there are simply accounts where the total amount increases or decreases within a journal entry. Each journal entry involves two accounts.

Using this accounting program begins with entering the opening balance. Here is how the opening balance is recorded:

For an account with a bank balance, the amount should increase, and for the account with the opening balance, the amount should also increase. This results in an increase in the balance. The amount recorded in the journal entry is also transferred to the final balance sheet account.

When you enter the opening balance of a credit, the amount in the credit account should increase, while the amount in the opening balance account decreases.

This constitutes an asset exchange—specifically, an exchange of balance sheet items—because the borrowed amount is already held in the bank account. The amount specified in the journal entry is not reported in the closing balance sheet account.

The opening balance of income and expense is not entered.

The program records three types of business transactions:

An increase in assets/liabilities occurs when the balances of two accounts rise and the accounts involved are either two balance sheet accounts or one balance sheet account and one revenue account. This happens, for example, when taking out a loan or transferring wages. The total amount in the final balance sheet account increases.

A reduction in assets occurs when the amounts in both accounts are decreased and the accounts involved are either two asset accounts or one asset account and one expense account. This happens, for example, during loan repayments or the purchase of household goods. The amount recorded in the journal entry is deducted from the final balance sheet account.

An asset exchange occurs when the accounts involved are two asset accounts, with the balance of one increasing and the balance of the other decreasing. This happens, for example, when transferring money from a bank account to a savings book account or vice versa. There is no change to the final balance sheet account.

The final balance in the program is not an account; the final balance is the sum of all increase in assets minus the sum of all reduction in assets.

P&L (profit and loss) is not an account here either; P&L is the final result of revenue less costs.

Incorrect booking entries can always be deleted; the password for deletion is the number 3.

Booking entries are always recorded in the selected month. The annual result is calculated after every booking entry.

The program can create multiple evaluations of the entered data.

Double-clicking a row in the list box with the left mouse button selects that row, and the data from the selected row appears in the combo boxes.

Before changing the year, you must access the current "Inventory accounts_list" report. The sheet containing the report should be saved as a PDF file.

When the year changes, a new calendar is created and all booking entries are deleted; the password is the number 3.

At the start of the New Year, the previous year's closing balance must be entered as the opening balance for all asset and liability accounts.

When entering the opening balance, note that for accounts representing assets (non-debt accounts), a positive annual figure is recorded as an increase in assets, while a negative figure is recorded as a decrease.

For accounts representing liabilities (debt accounts), the value is recorded as an exchange of assets/liabilities; the total opening balance figure decreases upon entry.

This is classified as an exchange because the amount owed is already reflected in the bank account.

The opening balance has been correctly recorded if the final balance of the previous year corresponds to the final balance of the New Year.